Britain will hold a referendum on June 23 to decide whether it wants to remain a part of the European Union (EU) or not. British PM David Cameron promised a referendum on this issue during his election campaign in 2015 as he felt that the EU had gradually evolved into a powerful bureaucracy that infringes on British sovereignty and issues of national importance such as trade, labour immigration, financial and labour regulations, and social spending. Major reasons which triggered Brexit issue are as follows:

- Net Contributor-The UK is a net contributor to the EU budget around 8.5 billion pounds per year. Click Here to Know More

- Immigration-The EU’s rules on free movement of labour have led to addition of 285,000 people each year (an increase of 0.4% in population) for the last 3 years which is creating social problems for Britain.

- Red Tape – Some of the EU rules such as maximum work hours of 48/week, same working conditions for full time and part time employees, etc apply to small businesses. This creates a large hole in their balance sheets.

Although the vote is not binding, the possibility of Brexit creates a lot of uncertainty for the EU. It can significantly impact trade, investment and economic growth in the region and weaken the bloc’s effectiveness.

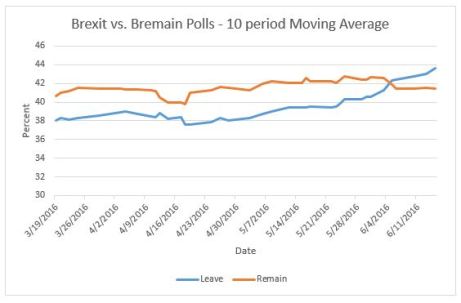

Escalating Brexit Fears

The Brexit polls have drawn significant attention in the financial markets for the past 3 months. Over the last 2 months, the 10-day moving average of Brexit polls has been increasing. Around the first week of June, Brexit fears escalated to such an extent that the Brexit polls trend line moved above the Bremain polls trend.

Source – Bloomberg

Note

1. Bloomberg Composite (Leave/ Remain) EU Index is calculated by taking an average of polls data from various surveys. The Composite Index does not include Brexit polls which do not report a value for the proportion of respondents who are Undecided.

2. The poll results are highly variable. Hence, taking a moving average gives an indication of the trend in sentiments.

Current Market Perception

Volatility has increased in the markets and investors are being more concerned. This can be explained by the following indicators:

- Libor – OIS Spread : As the uncertainty increases, LIBOR increases as banks will be skeptical to lend. The OIS is the overnight rate and hence can be considered to be almost risk free in the UK’s case. The greater the spread (difference), the more the uncertainty. While the LIBOR-OIS spread has been fairly consistent around the world, the UK LIBOR-OIS spread has widened starting mid-April. This indicates rising concerns for the UK’s economy. Click Here to Know More

- GBPUSD (3 month option) volatility and FTSE 100 Vol index – In anticipation of Brexit, the markets saw significant pressure in the GBPUSD currency pair and FTSE 100 Index. This is evident from the spurt in the 3-month GBPUSD Vol and FTSE 100 Index Vol around the first week of June.

Source – Bloomberg

Note – The FTSE 100 Volatility Index represents the implied volatility on the FTSE 100 Stock Index. The GBPUSD 3-month Vol uses the at-the money option implied volatility

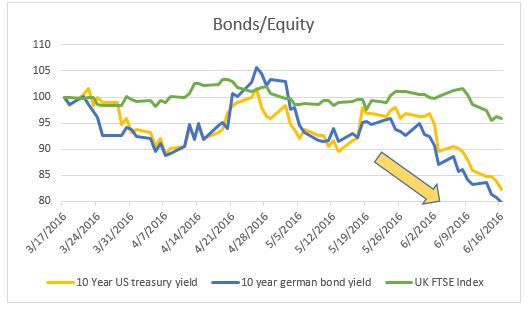

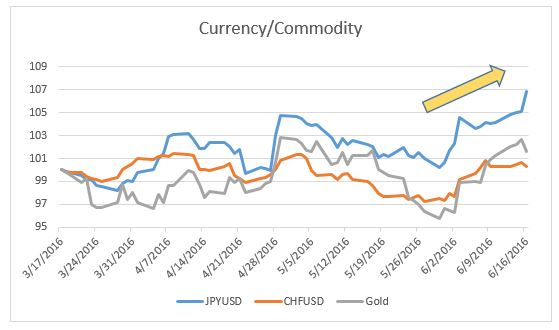

Movements across Major Asset Classes

This is clearly a risk-off situation. In a risk-off scenario, investors are expected to move from risky assets towards safe haven assets. The appreciation in safe haven assets has been significant over the last 2-weeks which coincides with the escalation of Brexit fears. This is complemented by an outflow of funds from the UK FTSE Index.

| Asset Class | Item | Movement observed |

| Currency | JPYUSD/CHFUSD | JPY and CHF have appreciated |

| Commodity | Gold | Appreciated |

| Bonds | US Treasury/German Bund | Yields have gone down. (Prices have increased) |

| Equity | UK FTSE Index | Index has fallen |

Note – The graphs below have been adjusted to a base of 100 as on 17/3/2016. Hence, a value more than 100 means that respective asset is appreciating.

Source – Bloomberg

Implications of Potential Brexit

Trade Impact

45-50% of the UK exports go to the EU. Additional tariffs will be imposed with the main implications being on the automobile and aircraft sectors. The uncertainty regarding the trade model that Britain will follow – the Norwegian, Swiss, WTO models or create its own model – is what is concerning Global CEOs. (Click Here To Know More (Page 6))

Financial Impact

Uncertainty around the UK’s trading regime is likely to defer investment decisions and limit household spending. Brexit will impact both Britain and the EU. We expect the BOE and the ECB to ease rates and initiate some temporary liquidity programs to induce growth.

On the currency front, GBPUSD is expected to depreciate by around 15 -20%. Current account deficit of 7% of GDP and potential reduction in foreign direct investment are the major factors that might amplify currency depreciation.

Chain Reaction

We expect David Cameron to resign because he firmly wants Britain to stay in the EU as it will help in maintaining its economic relations with the rest of the world. It is expected that other countries such as Denmark, Spain and Portugal might not hold referendums to exit, but hold referendums against specific EU clauses, thereby aggravating problems for the EU.

(All the views expressed are opinions of Punit Parekh, Shreya Aggarwal and Dinkar Mohta – Finance enthusiasts at IIM Bangalore)

The illustrations for the spread, Implied vol and a shift towards the safe haven assets correctly and quite comprehensively indicate an imminent downside for the Brit economy and/or currency (as aptly inferred in the article here). So how do u think this reconciles with the fact that Brexit was infact intended to curb the undesired policies against Britian ( rampant immigration inflow, undesired economic outflow and unsolicited infringement)?

The proponents of Brexit, in my opinion, have fair arguments suggesting the costs incurred by Britain to remain a part of the EU. However, the potential benefits of Brexit (the very reason for the campaign) are contingent upon the trade model to be adopted by Britain. This model will define the relation between Britain and the EU. There is substantial uncertainty regarding the choice of model.

The financial markets’ response indicates the short-term risk to the British economy in anticipation of Brexit. However, it is important to appreciate that the overall risk-off scenario, capital outflow, and currency depreciation are primarily because of the uncertainty surrounding the future course for Britain in the event of Brexit.

Hence, the uncertainty regarding the future model reconciles the pros and cons (mainly the financial markets impact) of Brexit.

The arguments about the costs incurred by Britain to remain a part of the EU are not fair at the least but a misleading play of numbers. The Brexit campaign argues Britain would save the GBP 19bn it now pays to be part of EU. What they don’t say is that GBP 5mn comes back as regional grants. The remaining GBP 14mn is approximately 1% of the government’s spending. Also, the potential loss of tax revenues in case of Leave scenario will be more than GBP 8mn, the IFS estimates. So, overall, there will not be much of a ‘saving’ through Brexit.

That said, I agree that the outcome of Brexit on trade is totally contingent on the trade model adopted by Britain. But we do have to keep in mind that Germany will not be very keen on giving favourable terms in fear of encouraging an exodus from EU.

Continuing on trade; 48% of Britain’s exports are to EU. While 16% of EU’s exports are to Britain. No brainer where the power lies. Classic case of big merchant-small customer arm twisting.

48% of Britain’s FDI inflows are from the EU. These obviously wouldn’t stop completely but will witness a dip. Unlike trade, the outcome of FDI dipping or plateauing is not contingent on a model to be adopted by the government but rather a whim of the foreign investors.

Leave campaign claims reduction in immigrants as it will curb the free flow of human resource between EU members. Historically, Non EU immigrants have been more than EU immigrants. (Source: http://www.migrationwatchuk.org/statistics-net-migration-statistics/#create-graph)

Among the arguments of the Brexit campaign, one that holds some ground is regaining some of their lost sovereignty (read: lesser regulation). In a isolated, unconnected world, I’d agree to that. But in these times of global interdependency and aligning to groups to increase negotiation power, a little compromise on sovereignty is necessary.

Labour unions and the working class are now waking up to the fact that leaving the EU will mean scrapping the cushy limit on work hours/week and minimum wages.

Overall, the arguments of the Brexit are very weak. The negatives are certain while the positives are contingent on many variables. And the markets have priced in these negatives.