In the last couple of years, there has been a lot of debate about what is best when it comes to fiscal stimulus – Money Financing (Helicopter Money, Printing Money) or Bond Financing (Selling Bonds), with one group of eminent economists supporting the former while another group pushing for the latter. To be able to understand the validity/rationale behind their theories, it is very important to understand the transmission mechanism via which the two methods work.

Let’s first consider Bond Financed fiscal stimulus. Bond financing basically refers to the combination of sale of government bonds/asset backed securities by govt/banks and the purchase of those bonds/ABS by the Central Bank. So how is this supposed to stimulate the economy? Well, asset purchases cause the bond prices and asset prices to increase. When the value of these assets increase, the holder of the assets experiences gain of wealth (also called “wealth effect”), and would tend to increase their consumption of ordinary goods and services. Moreover, the increased demand for bonds/assets would cause the long term interest rates to drop, and the reduce rates would then spur private investment. Both these effects together are expected to stimulate the economy and move it away from recession. Whether this “purported transmission” actually happens or not is debatable and we will talk about this later. But before that, let’s look at the other side of the coin – Money Financed Fiscal Stimulus. Money Financing or what many call the Helicopter Money Drop, basically means printing money to finance deficit/debt. Unlike bond financing, money financed fiscal stimulus doesn’t build up public debt. Also, proponents of this theory point out that while Bond Financing causes crowding out of private investment, the Helicopter Money mechanism has minimal impact on interest rates and creates a minimal inflation threat when applied in periods characterized by falling aggregate demand, excess capacity, deflation tendencies and high unemployment (Source: Economonitor). Again how much truth lies in this assessment is also subject to debate.

Let’s try and do a post-mortem of the different view-points expressed above.

a) “Bond Financing,via both these (wealth effects and increased investment) effects together is expected to stimulate the economy and move it away from recession” . Well do we really think this is the case!! Bond Financing supported by LSAP/QE directly impacts just the asset prices and increases the “high-powered money” but has no impact whatsoever on the money supply or the demand for goods/services. According to Richard Wood (on Economonitor), this asset price reflation benefits only the banks, speculators, traders and hedge funds, etc, (who have low marginal propensity to consume) and not the ordinary household/consumer. Thus, it’s difficult to believe that bond-financed (supplemented by QE) is any better in stimulating demand.

b) “Bond Financing causes crowding out of private investment, while Helicopter Money has minimal impact on interest rates and creates a minimal inflation threat when applied in periods characterized by falling aggregate demand, excess capacity, deflation tendencies and high unemployment ” Well, according to me this is like comparing apples and oranges. The idea that bond financing will cause crowding out of private investment is true only if the economy is running near full capacity (which would imply a vertical LM curve and thus, increased government borrowing would just cause the rate to rise, causing private spending to decline). But at times of recession, the economy is often in a state of high unemployment, and excess capacity. Under these circumstances, the government spending is very unlikely to raise interest rates, and is rather likely to raise output and “crowd in” investment.

So, in the backdrop of the evidences put forth by our post-mortem analysis, it seems that both the proponents seem to be missing an underlying point, which challenges their “purported” theories and also undermines the “purported” divergence between the two theories. So, we are back to square-one!! How are these theories different, or are they different at all? I must admit that I lack any professional experience to provide an alternative explanation but Paul Krugman’s theory (actually a lot of economist including Larry Summers seem to believe in this version) seems to make a lot of sense. This is what it is –

“So, compare two cases. In case 1, the government runs a budget deficit, which it finances by selling bonds to banks … At the same time, the central bank — an arm of the government — is engaged in quantitative easing, buying bonds from banks with newly created monetary base… But now consider case 2, in which the government pays for deficits simply by “printing money”, that is, adding to the monetary base.

How do these cases differ?

At the end of the day, the government’s financial position is exactly the same: debt held by the private sector is the same, and so is the monetary base. The private sector’s balance sheet is the same too. The only difference is that in case 1 banks briefly hold some government bonds, before selling them back to the government via the central bank. Why should this matter for, well, anything? “

Does this not make a lot of sense!! Exactly what our post-mortem analysis suggested !! There doesn’t seem to be much significant divergence between the two theories!!

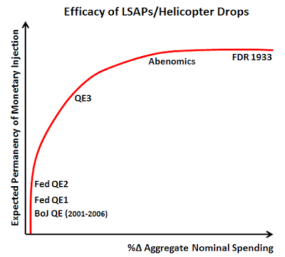

So then what matters!! According to Krugman “What you need to get monetary traction is to convince everyone that the monetary base will stay larger — to credibly promise to be irresponsible.” Prof David Beckworth of Kentucky University, has made a similar point in his blog. He says that as long as the central bank is able communicate its commitment to permanent expansion of monetary base, it does not matter whether one does helicopter drops or large scale asset purchases. As can be seen from the chart below, we can see why the US QE program has failed to gain much traction, as the programs were clearly indicated to be temporary. On the other hand, Abenomics -with its colossal monetary base expansion- has tried to communicate permanency of monetary stimulus and thus has been able to stimulate aggregate demand much more than their American counterparts.

In words of Beckworth, All of these experiences paint a picture of the relationship between the expected permanency of monetary base injections and aggregate demand growth.

Source: David Beckworth’ blog

– Akshat Kumar Sinha

References

1. http://mainlymacro.blogspot.in/2012/09/why-not-finance-fiscal-stimulus-by.html

2. http://macromarketmusings.blogspot.in/2013/12/the-wrong-debate-helicopter-drops-vs.html

3. http://www.economonitor.com/blog/2013/06/money-financed-or-bond-financed-fiscal-stimulus/