“One reason inflation is so destructive is because some people benefit greatly while other people suffer; society is divided into winners and losers. The winners regard the good things that happen to them as the natural result of their own foresight, prudence, and initiative. They regard the bad things, the rise in the prices of the things they buy, as produced by forces outside their control” – Milton Friedman

Blog by: Archana Maganti, Ayush Agrawal & Rishi Vora

Introduction

Inflation can be defined as too much money chasing too few goods. One of the primary reasons of inflation in developed economies is high government deficit (revenue – expenditure). If the government has a deficit, then this deficit is financed by external or internal borrowings. This leads to a rise in the incomes of the people and hence an increase in the aggregate demand which is given by the formula:

∆Aggregate Demand = 1/(1-mpc)*∆Income

MPC (Marginal Propensity to Consume): The marginal propensity to consume (MPC) is equal to ΔC / ΔY, where ΔC is change in consumption, and ΔY is change in income. If consumption increases by eighty cents for each additional dollar of income, then MPC is equal to 0.8 / 1 = 0.8.

Suppose a large corporation decides to build a factory in a small town and that spending on the factory for the first year is $5 million. That $5 million will go to electricians, engineers and other various people building the factory. If MPC is equal to 0.8, those people will spend $4 million on various goods and services. The various business and individual receiving that $4 million will in turn spend $3.2 million and so on. Hence this will form an infinite GP with r<1.

If the marginal propensity to consume is equal to 0.8 (4 / 5), then the multiplier can be calculated as:

Multiplier = 1 / (1 – MPC) = 1 / (1 – 0.8) = 1 / 0.2 = 5

We can see that, a change in income can lead to a much high change in aggregate demand (due to multiplier effect). Hence though inflation leads to no increase in the intrinsic value of goods or services, the demand for those goods and services increases thus leading to an increase in nominal prices. Depending on how the newly printed currency has been circulated, some would be able to afford the goods and services at the cost of others. In this blog, we will delve into the ‘bad’ of high inflation – how it promotes inequity in India – and later conclude by providing a strategy to counter these ill effects (in the follow-up blog).

Inflation – An added tax

Inflation is regarded as a case of taxation without representation or legislation. From the government’s point of view, inflation is essentially a monetary seigniorage (difference between the value of money and the cost to produce it) which acts as a source of revenue for the government. As the total value of assets remains constant, the government (currency issuer) is earning revenue at the cost of people (currency holders). Generation of new currency thus decreases the value of the existing currency (purchasing power), redistributes the resources in favor of government and acts as a hidden tax on the existing currency holders. This ‘inflation tax’ is then used by government to finance its debt, lower public expenditure in real terms and inflate GDP figures. (To know more about seigniorage in India, refer to the following link)

In a country like India, with dominant saving philosophy, millions of people particularly the poor who have no access to financial markets and pensioners who favor stability over risk, deposit money in savings accounts where nominal interest rate is generally lesser than inflation. Thus they end up paying this added tax to government every year.

Inflation – Effect on other taxes

Adam Smith laid down equity as the guiding principle of fair taxation: people should pay taxes per their ability to pay and marginal utility. However, inflation tax overrides this canon of taxation. Apart from acting as a tax itself, inflation also has a considerable impact on direct taxes i.e. ‘bracket creep’. For example, a year back a person who used to purchase a basket of goods at 2 Lakhs may not have been qualified as a tax payer, but at the current inflation rates, a person purchasing the same basket of goods at 2.5 Lakhs is now falling in the tax bracket, and has to lose his purchasing power in the form of taxes.

Iniquitous ‘Inflation Tax’

NSHIE Survey

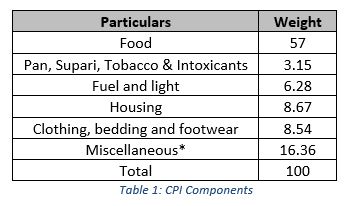

The various components of CPI and their corresponding weights as used in India are as follows:

From the above table, we can see that food prices form the biggest chunk in determining the value of consumer price index.

Inequity in impact of CPI fluctuations

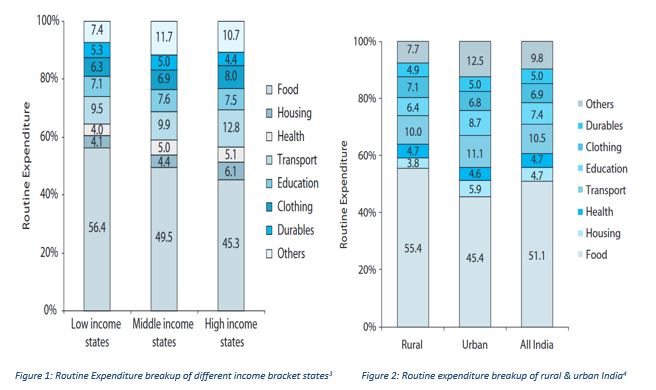

To compare the impact of inflation tax on different sections of the society, the percentage expenditure of these sections on different components of CPI have been compared using data from NSHIE survey. [1]

The following graphs illustrate the distribution of routine expenditure across various components for low, middle, and high income states [2] and for rural and urban population:

As shown above, low and middle income states have a much higher component of food in their total routine expenditure when compared with the high-income states. A similar trend can also be seen in the rural versus urban divide. Since food forms the biggest component driving CPI, it can be said that the impact of a higher ‘inflation tax’ is higher on low and middle income states as compared to high income states. Thus, we can safely conclude that inflation as a tax is iniquitous in the economy because not only does it act as an extra tax on the citizens but also because it is unequally distributed across various sections of the society.

However, we believe that CPI cannot be taken as a blanket measure of inflation for all income groups. Instead the government should look to develop different indices for different income groups where the weights would be decided based on sensitivity of that group to different components. This would help in capturing the impact of inflation on each income group better and thereby build policies around it. The overall inflation can be taken as the weighted average of the three indices where weights would correspond to percentage population in each group.

Inequity in generating returns from savings

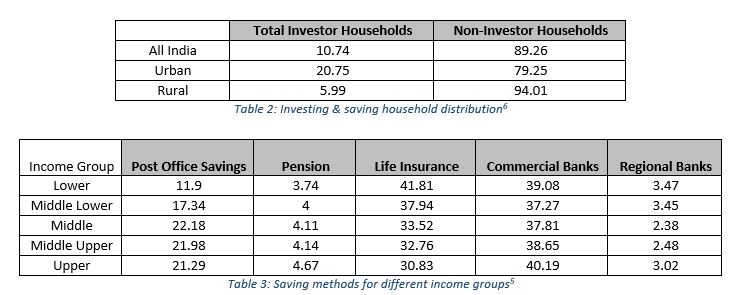

Based on a NCAER household survey, it has been found that the percentage of investors is nearly 20% in urban areas while it is much lower (6%) in rural India.[4] At an overall level, less than 11% of the total households invest in the market. This shows that the number of savers form a huge proportion of the total households in India. The following tables list down the distribution of investors (in %) in rural and urban India as well as various modes using which the households save their income.

From the above tables, we can say that a higher inflation would erode the savings of both rural and urban population. This is because both urban and rural households save majorly through life insurances and savings accounts in commercial banks which provide low/no returns. It can also be seen that the lower and middle lower income groups save much more (in % terms) through life insurance which generate no returns. Thus, the impact of high inflation would be much higher on rural households as compared to urban households.

Though investments generate higher returns as compared to savings, some of the major reasons why Indians prefer saving instead of investing are:

- Inadequate returns

- Not sure about the safety of investments

- Investments not very liquid

- Inadequate information

- No skills

- Dissatisfied with the role of regulator

- Inadequate financial resources

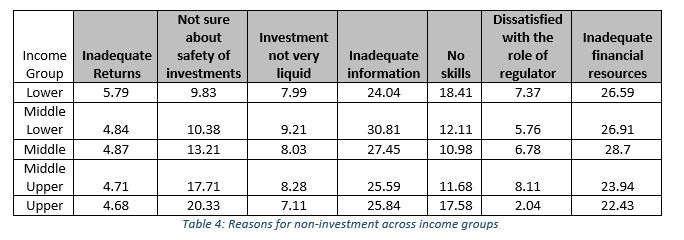

The following table lists down the weights (in %) of various reasons that non-investors attribute to their behavior

As can be seen, majority of the non-investors do not invest because of information asymmetry or because they have inadequate financial resources. This goes to show that lack of investments in India are due to factors which cannot be changed by spreading awareness about the benefits of investments or by making the investment systems more robust, safe or easy.

Conclusion

So far we have established that in Indian economy, the impact of high inflation (>5%) on different sections of the society is inequitable. Therefore, keeping inflation under control should be at the heart of fiscal and monetary policies of the economy. A failure to do so stands to bring the general public in cross-hairs with the government thereby disturbing the economic stability in the long run.

The government and RBI should curb the negative implications of high inflation by ensuring fiscal and monetary prudence. To know how we think this can be done, keep following “Macro in a nutshell” for the next blog on recommendations.

Disclaimer – All the views expressed are opinions of Networth – IIMB Finance Club – members. Networth declines any responsibility for eventual losses you may incur implementing all or part of the ideas contained in this website.

References

[1]http://www.thesuniljain.com/files/thirdparty/NCAER%20How%20India%20Earns%20Spends%20and%20Saves.pdf

[2] Low income states: Assam, Bihar, Madhya Pradesh, Meghalaya, Orissa, Rajasthan, Uttar Pradesh, Chattisgarh, Uttaranchal and Jharkhand; Middle income states: Andhra Pradesh, Himachal Pradesh, Karnataka, Kerala, Tamil Nadu and West Bengal; and High income states: Goa, Gujarat, Haryana, Maharashtra, Punjab, Pondicherry, Chandigarh and Delhi

[3]http://www.thesuniljain.com/files/thirdparty/NCAER%20How%20India%20Earns%20Spends%20and%20Saves.pdf

[4]http://www.sebi.gov.in/cms/sebi_data/attachdocs/1326345117894.pdf

[5]http://www.sebi.gov.in/cms/sebi_data/attachdocs/1326345117894.pdf