Blog by : Arush Dixit, Ayush Agrawal, Koustav Mandal, Rishi Vora & Shivam Singhal

Yesterday, we discussed about the various factors which could prompt RBI to cut rates tomorrow. Today, we examine potential reasons for no rate cut followed by our take on the policy decision and a trade idea based on our view.

Why Status Quo?

We attribute the following as potential reasons for status quo by RBI:

- GST and 7th Pay Commission implementation: GST and HRA increase under 7th pay commission kick started on 1st As a result, their upside impact on CPI inflation is yet to be seen. Under this uncertainty, RBI might want to go for wait and watch approach until more data points are available. It is expected that the CPI inflation might increase by ~65 bps solely due to HRA increase as per a HSBC report. Also, CGST, IGST and SGST components in industries like entertainment, services, household products etc. which form a part of CPI basket have increased which might put an upward pressure on CPI inflation.

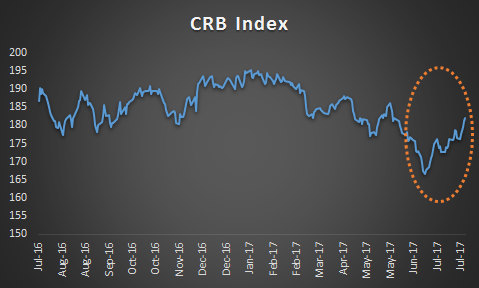

- Rise in commodity prices: Thomson Reuters CRB commodity index (an index to track commodity prices) comprising of crude oil, steel, aluminium, copper, coffee, cocoa, wheat, soya bean and other commodities shows that the commodity prices have rebounded. This increases the possibility of costlier raw material imports in near future thereby posing an upside risk to CPI inflation. The following figure illustrates CRB index time series data:

- Twin deficit problem: The RBI deputy governor Dr. Viral Acharya, in his recent comments mentioned NPA resolution as the top priority for the apex bank. The gross NPA of Indian banks rose to 9.6% in March 2017 from 9.2% in September 2016 as per RBI data. This reduces the probability of rate cut as RBI would want to focus first on structural issues to improve the policy rate transmission mechanism. At the same time, the balance sheets of corporates are over leveraged which is deterring them from borrowing. Due to this twin deficit problem, we might see a cautious approach from RBI.

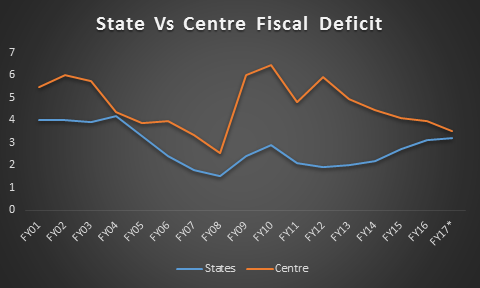

- Rising state fiscal deficit: Over the past 5 years, state fiscal deficit has been on the rise and recently, it has converged with the centre’s fiscal deficit. Moreover, recently the government has provided farm loan waivers which will put additional pressure on the state fiscal balances. The total amount of farm loan waivers is ~Rs. 3.1 lakh crore which accounts for 2.6% of the country’s GDP. Not only will a higher fiscal deficit and hence a higher borrowing crowd out private investment, but it would also compel RBI to keep the policy rates unchanged so as to keep a check on state’s fiscal prudence by keeping higher debt servicing cost.

Conclusion

As we have seen from the above analysis, there are multiple factors at play which might sway RBI’s decision in either direction on 2nd August. Whatever happens, India Inc. and FIIs are expected to stay optimistic about India’s growth story owing to continuing structural reforms undertaken by both – a politically stable government and an independent RBI.

Apart from policy rate decision, a major focus of the Indian markets would be on the language/forward guidance as provided by the MPC. The MPC would also take into account the associated risks arising from balance sheet unwinding by the US Fed and tapering of quantitative easing by the European Central Bank. This would in turn set the tone for the future bi monthly monetary policy reviews.

Our Take

Repo Rate stance: After analysing all the factors as discussed above, we believe that RBI would go for a 25 bps rate cut to 6% on 2nd August. We also expect RBI’s stance to be neutral owing to structural problems in the economy which is hampering private sector lending. We believe that this might be the last opportunity in this fiscal year for RBI to cut policy rates and provide enough time for transmission to the banks as inflation at the moment is bottomed out.

Reverse Repo stance: The reverse repo rate at this point is 6% leaving no margin for RBI to cut policy rates by 25 bps. Therefore we believe, that the rate cut would be complemented by a 25 bps reduction in reverse repo to 5.75%.

CRR stance: No change in CRR as increase in CRR at this point might put pressure on already stressed banks. This should be the last resort to suck liquidity given the circumstances.

SLR stance: RBI is likely to keep the SLR unchanged as the banks are already holding significant amount of government securities (~29%) on their balance sheet.

Open Market Operations (OMOs): Since there is excess liquidity in the system as witnessed during the 6th July OMO operations conducted by the RBI which was 6 times oversubscribed, RBI would need to engage in multiple OMO operations in future to suck excess liquidity out of the banking system.

Trade idea

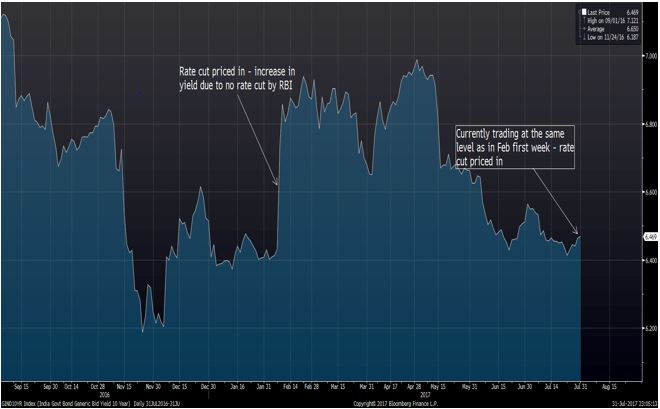

Back in the first week of February, we observed similar dynamics where a rate cut from RBI was priced in. Post February there has been no rate cuts and currently the benchmark 10 year yields is trading at a similar level implying the pricing in of a 25 bps rate cut. We feel that there is limited downside to the yields as we expect only one rate cut in this fiscal year. So, we recommend going short 10 year government securities i.e. yields to rise.

Entry level: 6.4%

Target Yield: 7% (high made since January’17)

Stop Loss Yield: 6.25% (based on 4:1 reward-risk ratio)

Horizon: 1 year

Disclaimer – All the views expressed are opinions of Networth – IIMB Finance Club – members. Networth declines any responsibility for eventual losses you may incur implementing all or part of the ideas contained in this website.