Blog by: Arush Dixit, Ayush Agrawal, Koustav Mandal, Rishi Vora & Shivam Singhal

The current state of the Indian economy is what we call as that of an “Optimistic Anxiety”. Not to be buoyed down by the current quarterly slump in the growth rate, the global bankers are still counting on India to bounce back and be the fastest growing economy in the world. This oxymoronic outlook arises from a medium-term euphoria countered by near term deflationary measures. The historic implementation of Goods & Services Tax (GST) with its potential of ‘One Country, One Market’, RBI’s & Government’s measures to mitigate the Twin Balance Sheet (TBS) challenge and the general confidence in the financial market about growing macro-economic stability has created a buoyant outlook for the economy in the medium term. However, this enthusiasm is curtailed by the more immediate problems of stalled Industrial production, increased demand for farm loan waivers and rising NPA’s in Public Sector Banks.

Goods & Services Tax (GST) will bring harmonization of tax laws and procedures across country creating a unified National market leading to ease of doing business. The GST regime should result in production efficiencies that could raise global competitiveness, improve profitability and increase GDP. Doing business in the country will be tax neutral irrespective of the place of doing business. GST would mitigate huge compliance cost incurred by the companies on complying with various indirect tax laws, administrative cost incurred by the Government, capture value addition and widen the tax base; it would generate a third-party paper trail and prevent tax evasion or black money circulation; and it would boost exports by making them zero rated. (To get a detailed understanding of GST, refer previous blog post here)

The government has also taken some key initiatives to Non-Performing Assets (NPA) of Public Sector Banks. New ordinances have been passed for amendment in banking laws to strengthen the Central Bank. The amendments give RBI the right to issue directions to any banking company to initiate insolvency resolution process in respect of a default under the provisions of the Insolvency and Bankruptcy Code. Recognizing that key to reducing NPA’s timely recognition of bad assets, new ordinances will enable RBI to take a call assigning final haircuts, where Rating Agencies or other independent evaluation could be mandated for banks to value specific NPAs and assign haircuts.

These initiatives by the government and RBI have led to positive outlook of the economy by the industry leaders and bankers. However, we should take this buoyant story of the Indian economy with a pinch of salt. The media and politicians are painting a rosy picture of India as the land of opportunities but it should not be believed blindly. Instead all these claims need to be backed by strong data. If we look at the Index of Industrial Production (IIP) which details the growth of various sectors like manufacturing, mining and electricity, the growth rate has seen a steady decline over the years with sharp drop in 2017 from ~5% to less than 2%.

Figure 1: India Industrial Production Trend (Source: CSO)

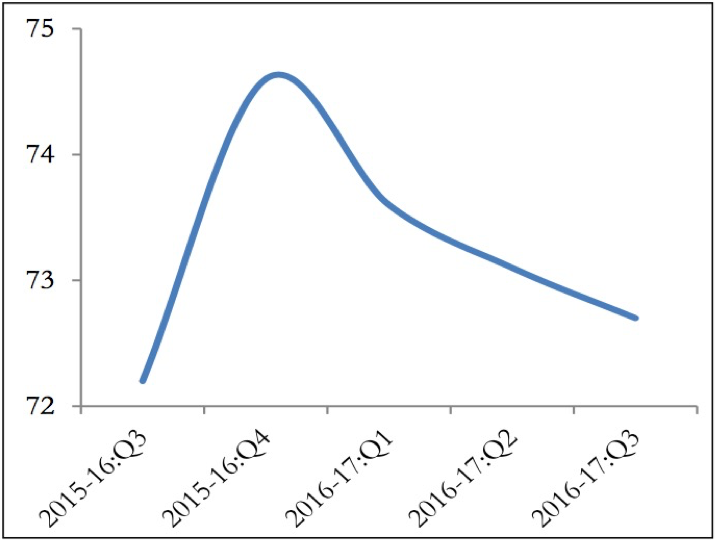

Capacity utilization rate, which indicates the buoyancy in production as well as potential future investments has also stalled at 72%, 8% below the high in 2010 at 80%. A low capacity utilization indicates that the existing industrial capacity is sufficient to meet the current demands of the consumers. Hence it reduces the scope for future investments in the industry.

Figure 2: Capacity Utilization Trend (Source: CSO)

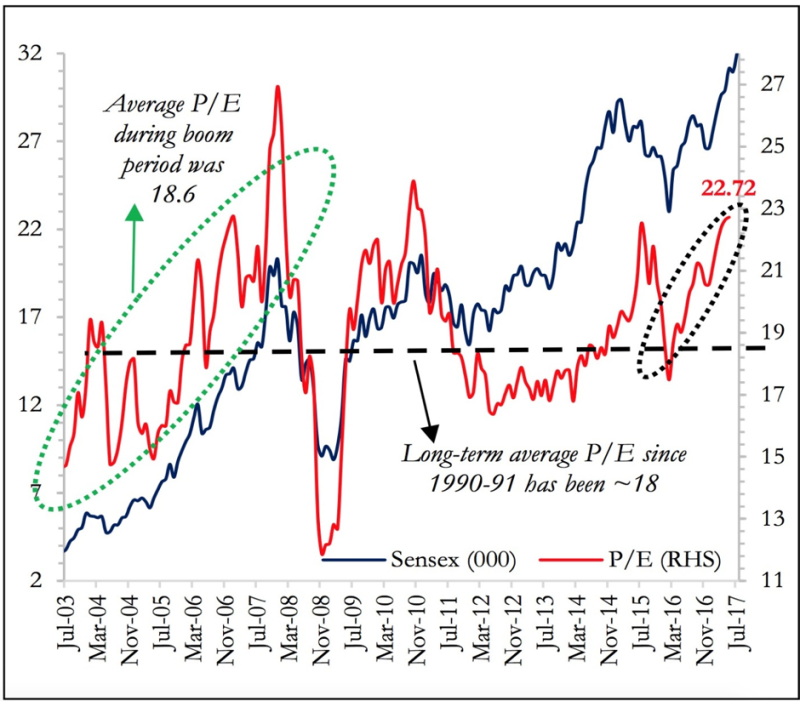

However, during this same time period the 10-year government bond yield is at close to the lowest value in past 15 years at 6.4%. As bond price and bond yield follow an inverse relation, this decline in yields imply higher bond valuation. Even more striking is the rally of Sensex in 2017 with an intra year gain of close to 11%. Even more striking is the high P/E ratio of the Indian stock market with NIFTY 50 going on an average of 24 and BSE at 23. These levels are the same as achieved in 2007 and are significantly more than the long-term average of 18. Such high P/E values can only be sustained if the investors feel that there is scope of future economic growth. If not then there is a strong tendency for reversion towards more realistic valuations as happened in the aftermath of 2008 recession.

Figure 3: Sensex & Price Earnings Ratio (Source: CSO)

Farm loan waivers have been announced by several state governments in line with their pre-poll promises and more will follow in the run up to 2019 elections. The farm revenues declined due to a decrease in price of non-cereal crops which were then further aggravated by consecutive droughts of 2014-16, resulting in a growing demand of farm loan waivers from major producer states. These waivers will further deteriorate the state finances which have already taken a hit after the power sector reform scheme UDAY. The increase in debts and liabilities of states will prompt the states to check their expenditures or increase their revenues by raising taxes to control fiscal deficit. The decrease in capital expenditures will have an adverse impact on economic growth.

The Economic survey 2016-17 by Ministry of Finance in its assessment states that farm loan waivers may increase public spending in the short run on the back of rise in wealth of farm households, but also warns that the negative effects of states cutting on expenditures may overpower the positive effects of increased farm households spending, thereby leading to reduced aggregate demand.

The question now arises is whether the promised growth outlook can be maintained. The Indian GDP grew by on average of 7.5% over the past 2 years against weak investments, production, export volume and credit. This poses a puzzle on the real reason of this stupendous growth. To tackle this puzzle, the Indian Economic Survey did a cross-country comparison of GDP growth and the aforementioned growth factors. They observed that in the past 25 years, there has never been a scenario of country growing by over 5% with the economic factors as that of India. This is in sharp contrast with the Indian GDP growth of over 7%. Hence it can be concluded that it’s not the exports and production but consumption that is driving the current growth phase. However, to sustain this current growth trajectory, action must be taken on the regular growth drivers of investments, exports and credit or else the GDP growth rate slump of 5.7% in Q1 will move from becoming a shock to the new norm.

We believe that to turnaround the economy, government needs to increase the amount of credit available to the industries. Currently the Public Sector Banks have shown slowdown in credit growth rate owing to higher NPA’s which has reduced the capability of Medium & Small Enterprises to make investments. Recapitalisation of Public Sector Banks by the government will enable them to drive the credit growth and ease the pressure from private sector which will help in driving the growth of economy. The government should divest some of its stake in these PSBs to raise this capital so as to not put additional pressure on its fiscal balance sheet.

Growth can also be fuelled by creation of new jobs and India, with the largest youth population in the world, has an immense scope in it. While growth revival through public spending will itself create jobs especially in the construction sector, it is also of great importance to focus on other labour-intensive sectors. The archaic labour laws should be revamped making it easy for the firms to hire and fire employees. This will enable an increase in fixed term employment compared to the current situation where workers work on a temporary contract basis.

Disclaimer – All the views expressed are opinions of Networth – IIMB Finance Club – members. Networth declines any responsibility for eventual losses you may incur implementing all or part of the ideas contained in this website.

Source: http://indiabudget.nic.in/e_survey2.asp