Blog by : Ayush Agrawal, Koustav Mandal, Rishi Vora & Shivam Singhal

RBI is going to convene for its bi-monthly monetary policy review on 2nd August 2017. The MPC would most certainly be divided in its opinion about the policy rate cut given plethora of macroeconomic factors that are currently playing in the domestic and global markets. This has kept the businesses and traders guessing about RBI’s stance and more importantly its forward guidance about the Indian economy. In this blog, we will analyse the various factors that might have significant role in determining RBI’s decision and come up with our recommendation and trade idea for the D-day.

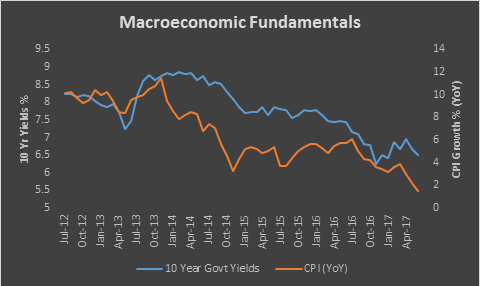

Historically, RBI has been accommodative in its policy rate decision since January 2015. The repo rates have been cut by 175 bps majorly due to stabilization of CPI at ~6% from a high of ~12% in 2013 and softening in the commodity prices due to global slowdown thereby prompting RBI to create a favorable ecosystem for pickup in investments. The following chart explains the shift in macroeconomic fundamentals of India since 2012:

As we can see from the above chart, both the 10 year government yields and CPI have shown a downward trend in the last four years indicating the accommodative stance of RBI.

Why Rate Cut?

We attribute the following as potential reasons for rate cut by RBI:

- Lower inflation (CPI) and surplus liquidity: The target band of CPI inflation is currently set at 2-6%. The latest CPI inflation number of 1.54% has deviated from the lower bound of the target thereby indicating a need for easing the monetary policy. The inflation numbers have steadily followed a downtrend with the last three data points below 3% mark. Also, there is surplus liquidity in the banking system and dismal credit growth, thereby increasing the need to spur investment. This can be made more probable by providing banks with higher margins (between lending and borrowing rate) through rate cut. Given the inflation numbers at this point are below 2%, RBI runs very low risk of overshooting the target band by cutting policy rates on 2nd August.

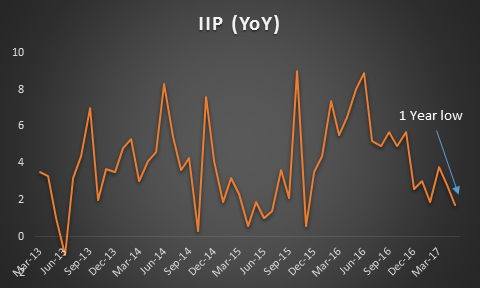

- Lower GDP growth and index of industrial production (IIP): There has been a decline in GDP growth rate to 6.1% against the market expectations of 7% YoY. The major reasons attributed to this slowdown are demonetization and decline in output in almost all sectors except agriculture which has led to one year low in IIP number of 1.7% against an expectation of 2.8%. A rate cut at this point would shift the IS curve (due to increase in investment) to the right thereby increase aggregate demand and hence the output in economy.

- Good monsoon expectations: According to the latest India Meteorological Department (IMD), the cumulative rainfall received till now is 103% of the benchmark long period average. This is attributed to the absence of El Nino. In India, the monsoon is critical to India’s farmers as it accounts for more than 70% of the total annual rainfall and recharges water levels in reservoirs in the absence of proper irrigation facilities in most regions. This would lead to increase in supply demand differential for food items which would keep the prices muted in near future. Since food component has a weight of ~46% in CPI basket, it is likely to put downward pressure on CPI inflation.

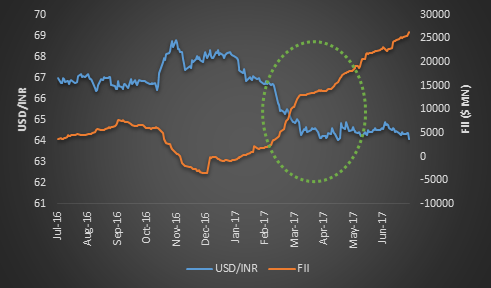

- Exchange rate and interest rate differential: USD/INR has depreciated (INR has appreciated) from ~67 to ~64.5 post UP election results due to greater confidence in the current political regime. This has resulted in higher capital inflows in the Indian economy. As a result, FII investments have increased to all time high of ~$26bn thereby further warranting the need for rate cut to drive up the investment sentiment and continue to boost foreign investments in India. Stronger INR would also make imports cheaper thereby reducing imported inflation.

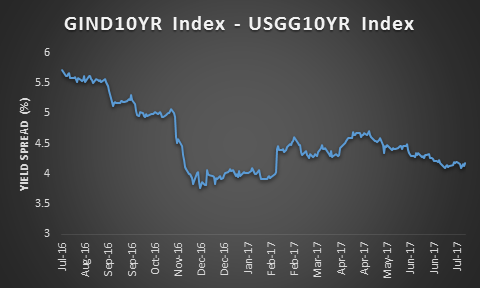

Despite the rate hike cycle in US resulting in a decrease in the interest rate differential in 10 year government yields between India and US, there has been minimal impact on the capital inflows in India. This shows that a rate cut by 25 bps at this point of time will not hurt the capital inflows given the optimism in investor sentiment owing to India’s growth story.

Despite the rate hike cycle in US resulting in a decrease in the interest rate differential in 10 year government yields between India and US, there has been minimal impact on the capital inflows in India. This shows that a rate cut by 25 bps at this point of time will not hurt the capital inflows given the optimism in investor sentiment owing to India’s growth story.

- Dovish Fed: As per the last FOMC statement, the Fed chair Janet Yellen was apprehensive about the inflation target. Therefore, we expect a dilution in the hawkish stance and Fed is likely to follow a wait and watch approach before taking any policy decision. Also, IMF has downgraded US GDP growth forecast from 2.3% to 2.1% in 2017 and from 2.5% to 2.1% in 2018 due to lack of action on promised policy changes by Trump administration. This further would reduce the chances of steeper rate hike cycle in the next financial year.

- Weak Capacity Utilization: Based on Order Books, Inventories and Capacity Utilization Survey (OBICUS), the capacity utilization has declined successively for three quarters during 2016-17 and stood at 72.7% in Q3 2016-17. Also, the below table shows that average finished goods inventories have been increasing and the Inventory/Sales ratio has also shown an uptrend indicating weaker demand in the market. Therefore, in order to spur demand and improve capacity utilization, we believe RBI should go for a rate cut.

In the subsequent part of our blog which would be published tomorrow, we would talk about why RBI could go for status quo on repo rates followed by our take on the policy stance that RBI should take. We would also recommend a trade idea based on our analysis. Do watch out for the next post from Networth!!

Disclaimer – All the views expressed are opinions of Networth – IIMB Finance Club – members. Networth declines any responsibility for eventual losses you may incur implementing all or part of the ideas contained in this website.